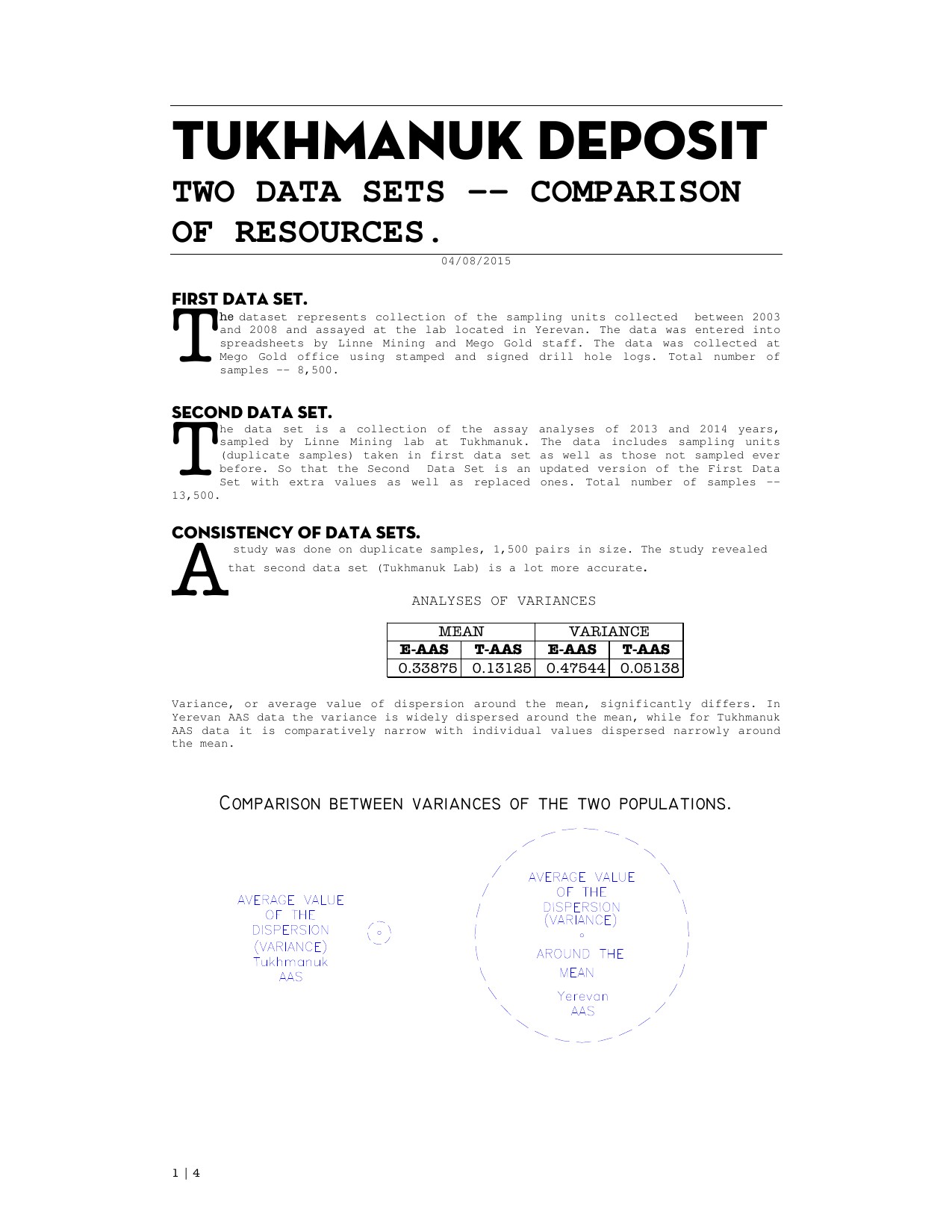

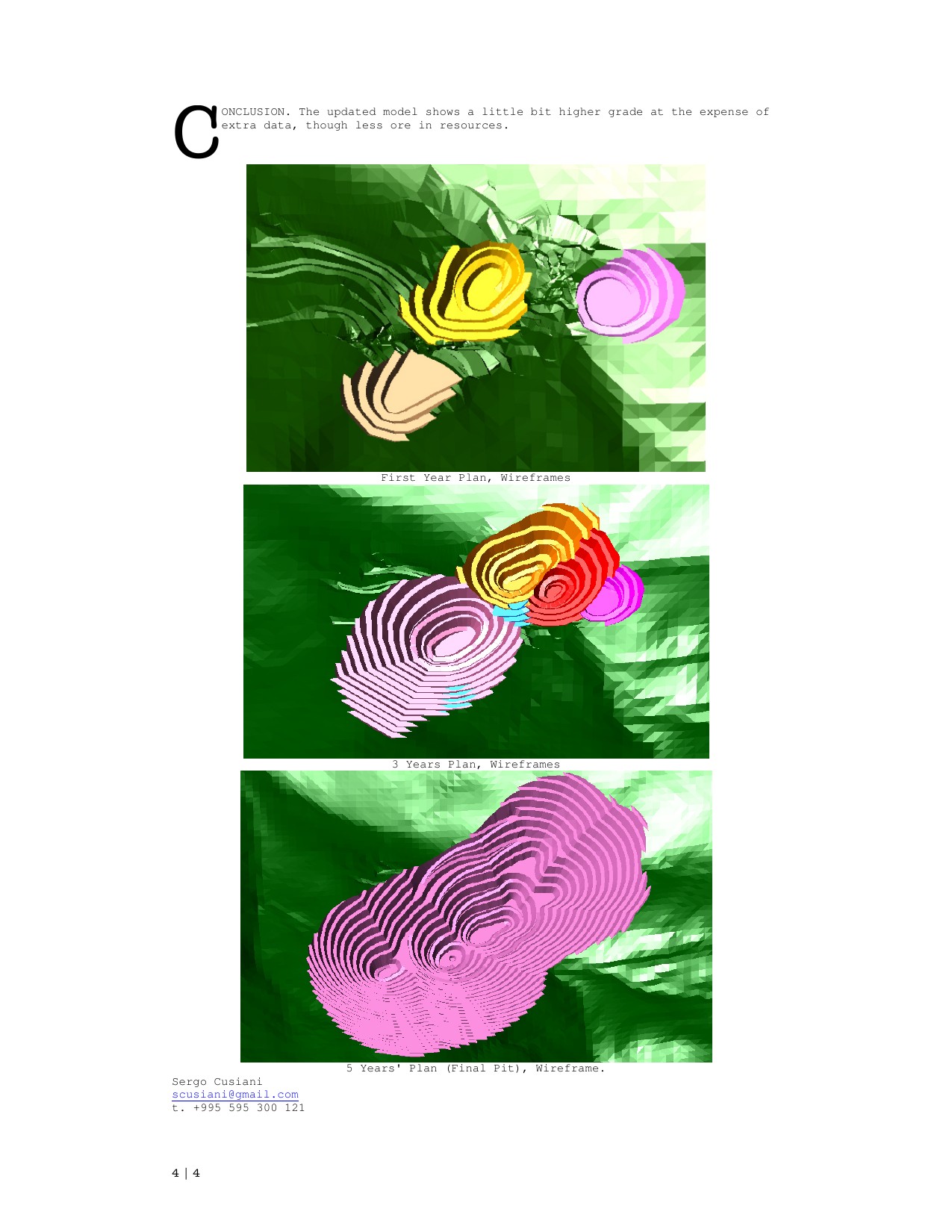

The arithmetic in the 2016 file reconciles. The problem is everything upstream of the arithmetic.

The Toukhmanuk mineral field, in Armenia’s Aragatsotn region, has been worked in

one form or another since the 1980s. In November 2016, the State Committee of Reserves

issued Expertise Conclusion N6, formally registering a reserves estimate

prepared by Mego-Gold LLC, the Armenian subsidiary of the

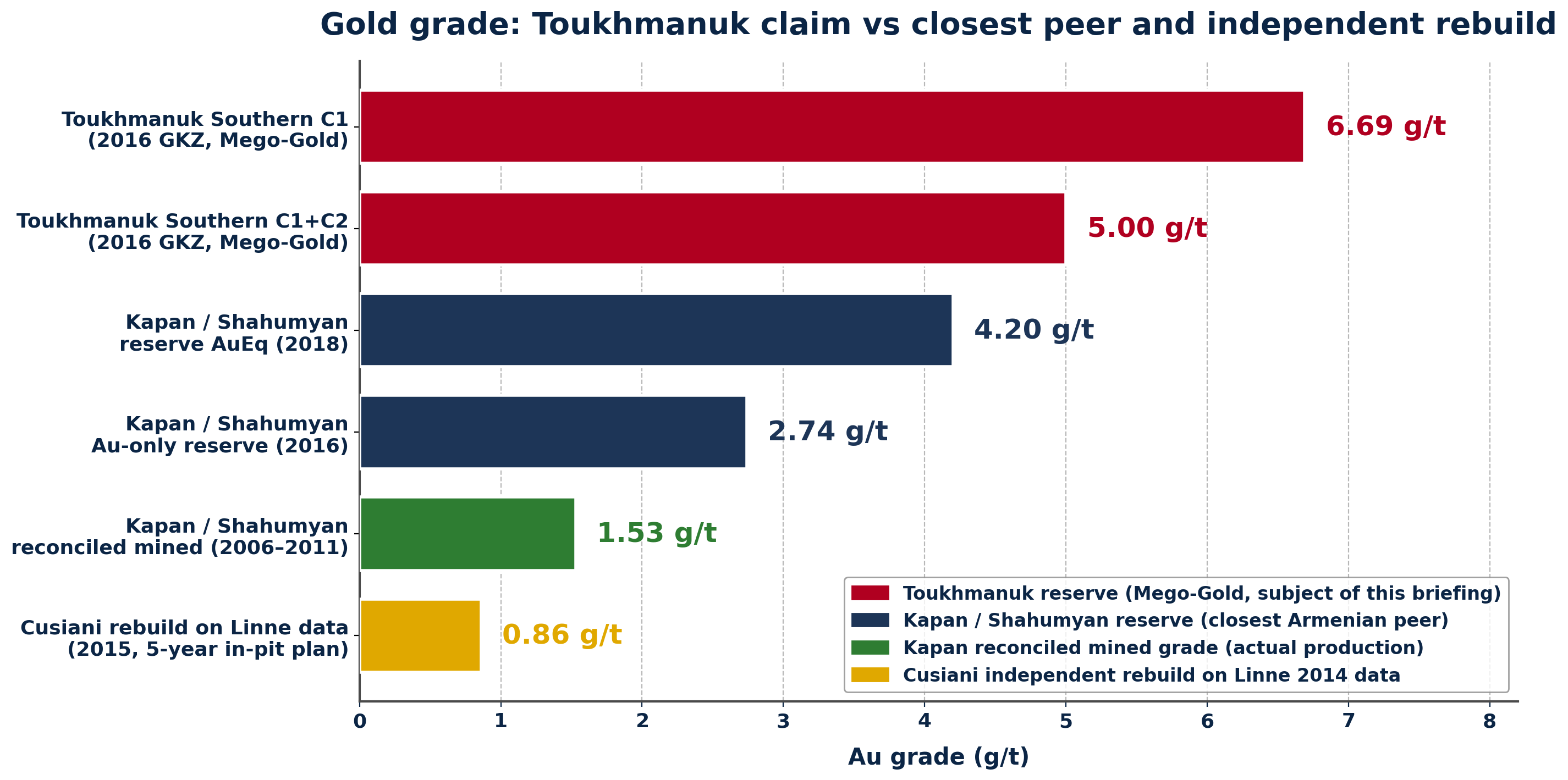

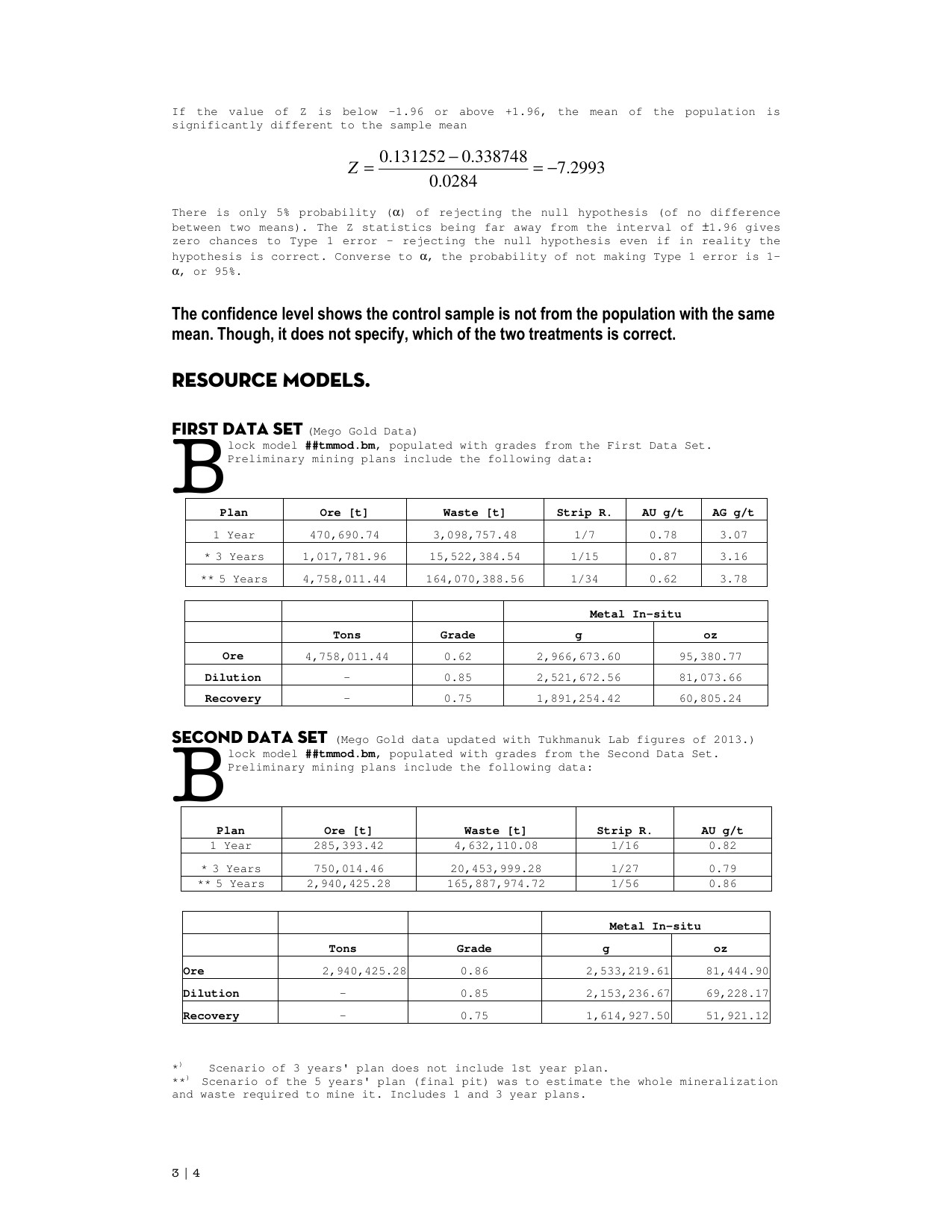

US-listed Global Gold Corp. (OTC: GBGD). The registered tonnage was 2.57 million tonnes

of ore; the headline grade, 5.00 g/t gold at the Southern area; the highest-confidence

category, 6.69 g/t.

Those numbers are arithmetically consistent with the block-level tables in the file.

Addition is not the issue. The issue is that the sample database on which

the block tables rest — the same database that earlier supported a much larger claim

in the 2011 Behre Dolbear

NI 43-101 technical report of 39.23 Mt at 2.1 g/t Au —

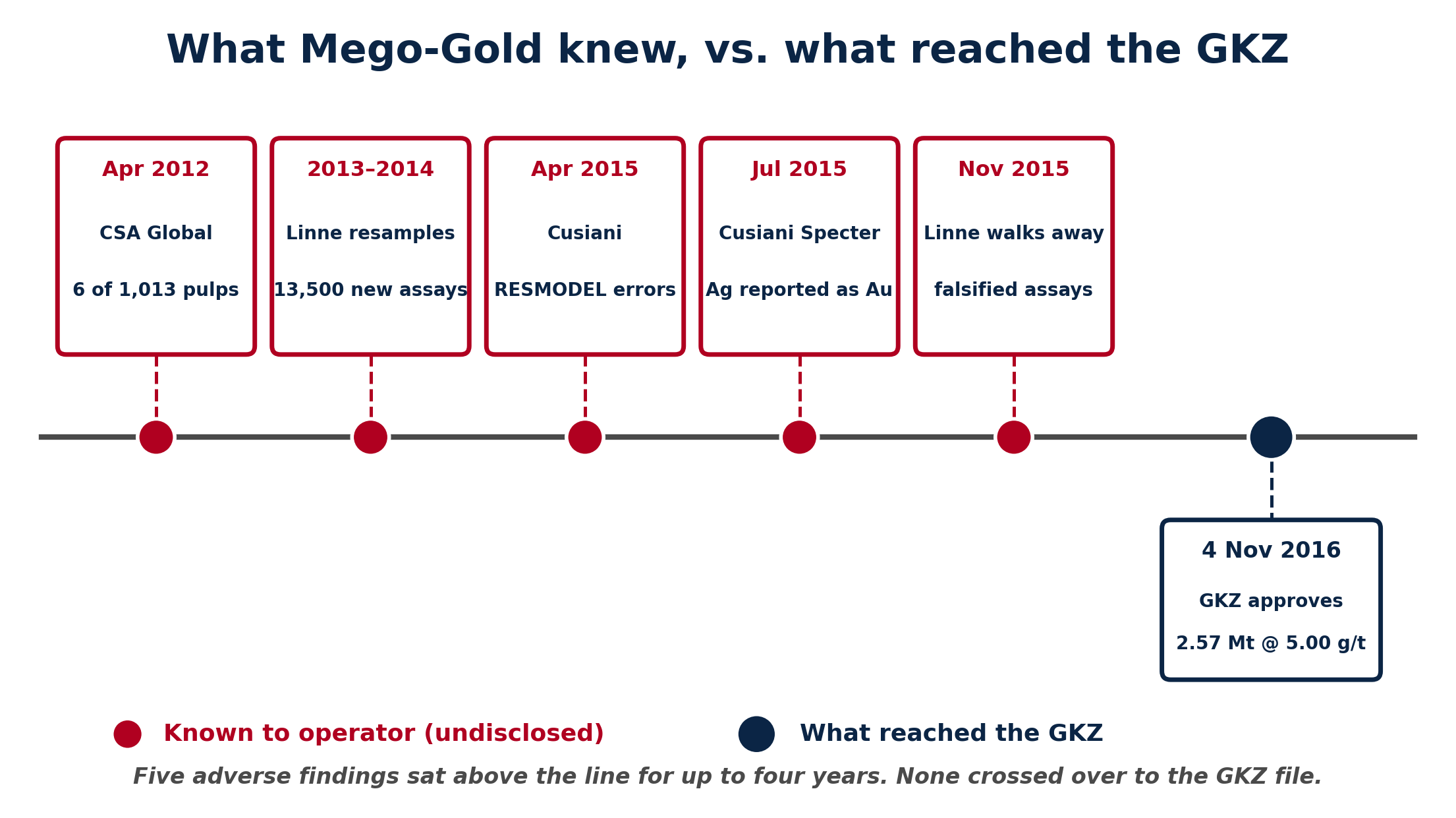

had, by April 2016, been the subject of two separate adverse

independent reviews, commissioned by two different commercial counterparties, over

the preceding four years. Neither review was placed before the commission.

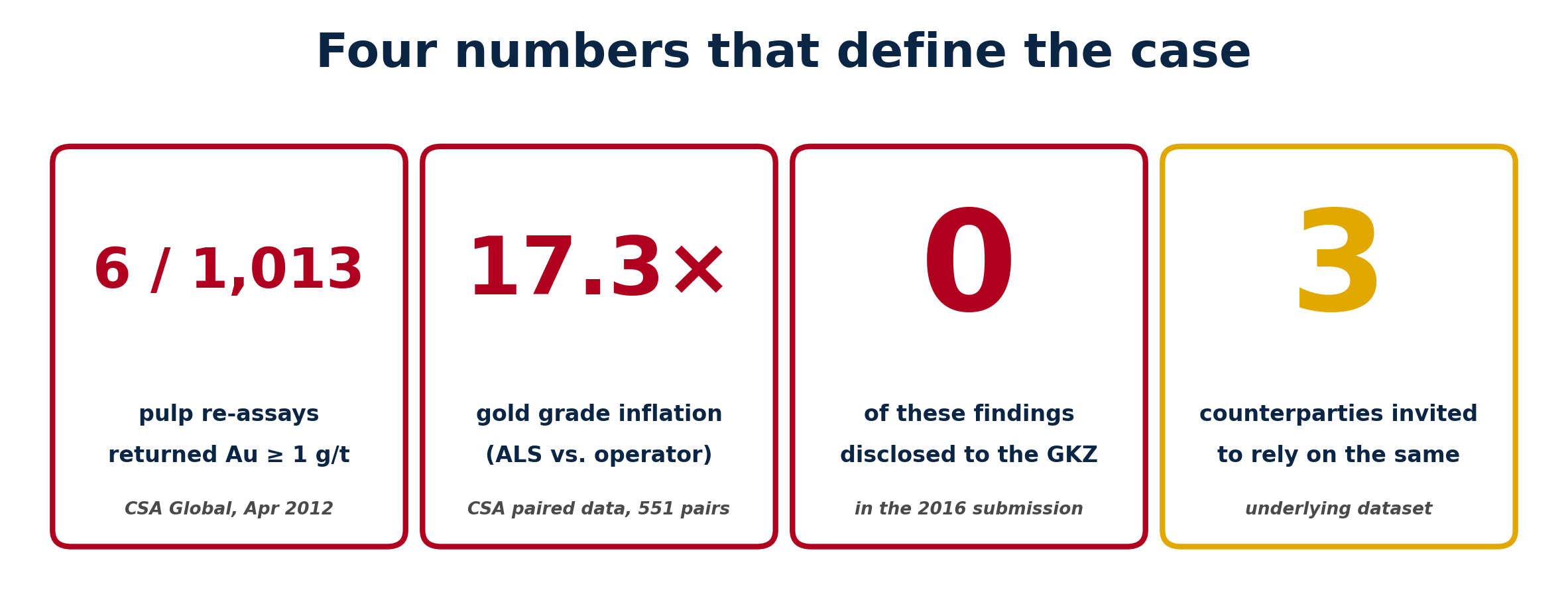

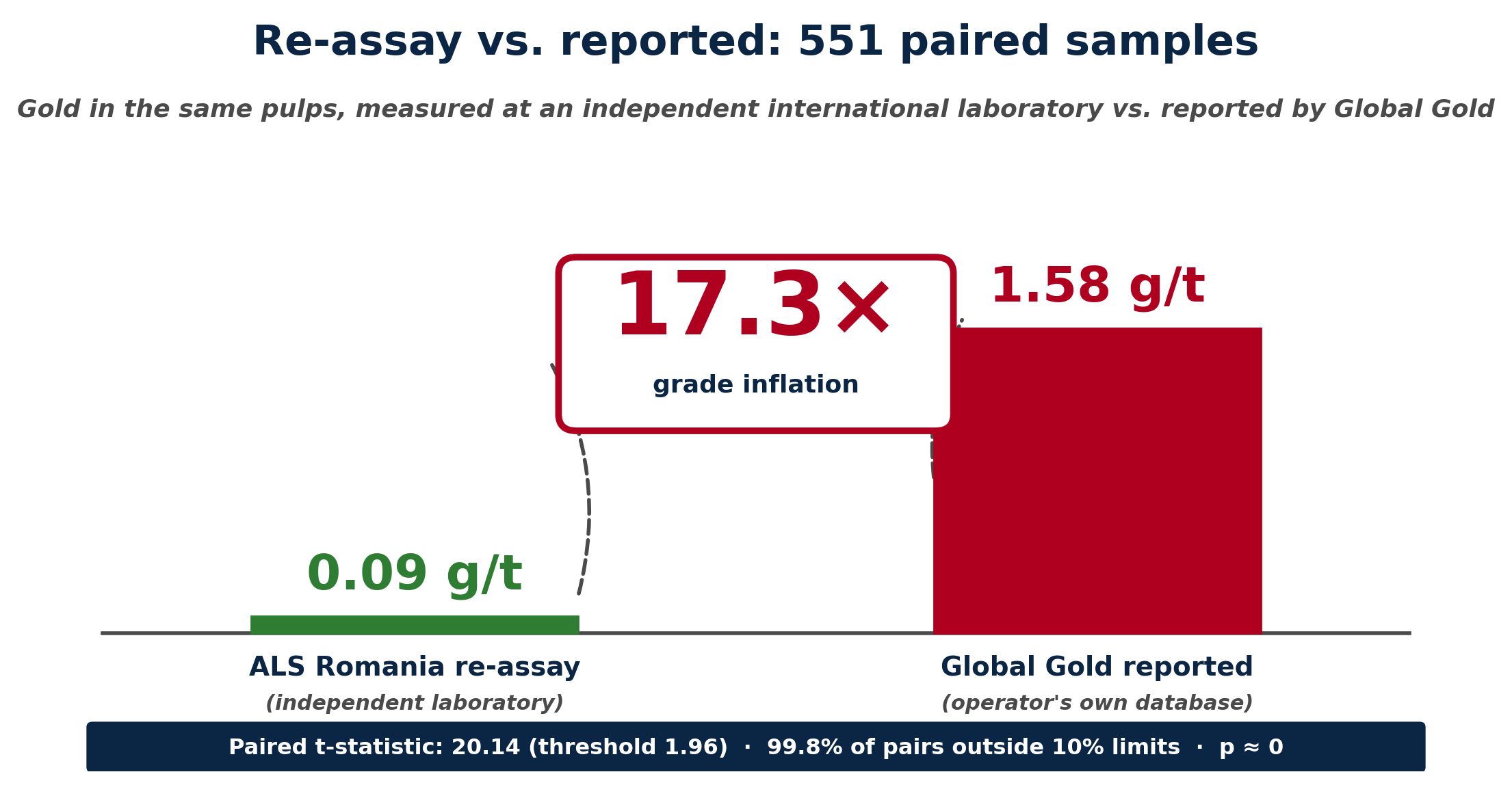

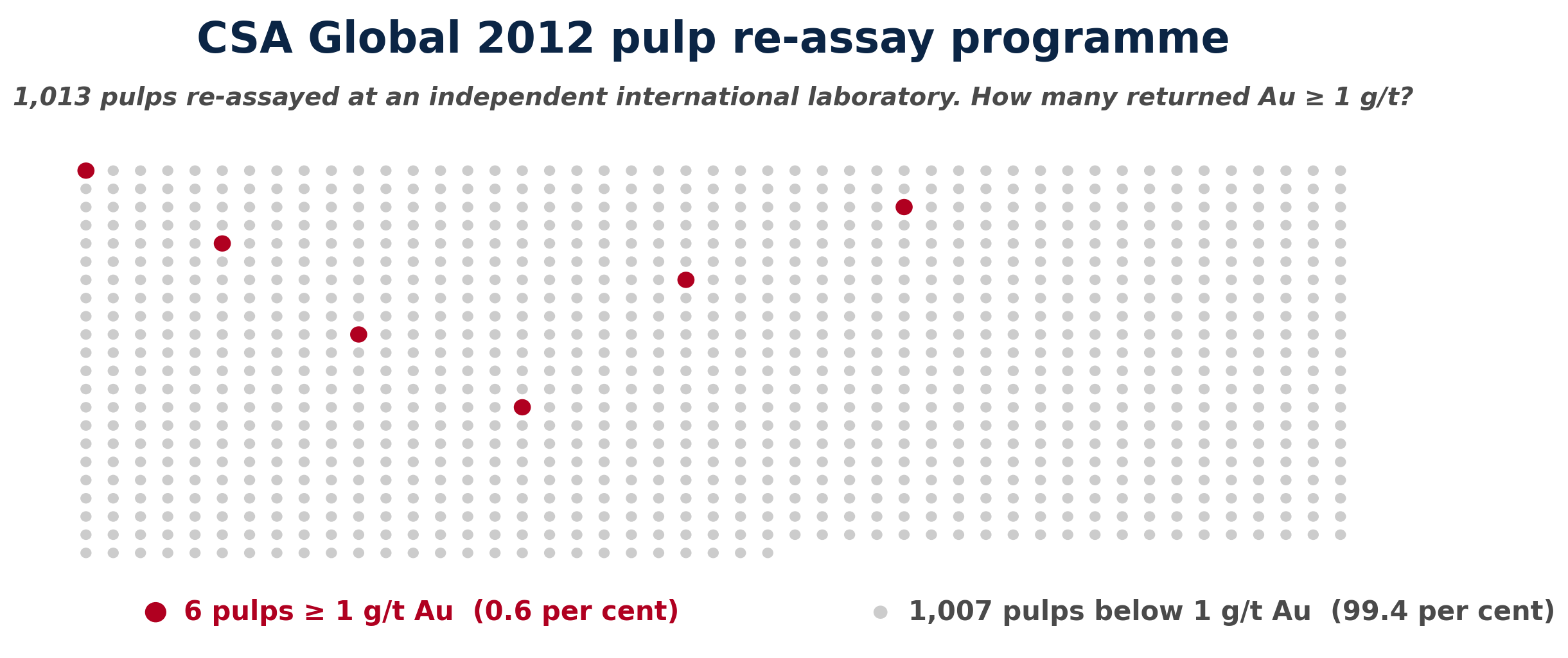

The first review, by CSA Global Pty Ltd. in April 2012, was a

re-assay of 1,013 pulp samples at an independent international laboratory (ALS Romania).

On the 551-pair subset with matched Global Gold database values, the mean gold grade in

the independent re-assay was 0.09 g/t against 1.58 g/t

reported by the operator for the same pulps — a 17.3× divergence.

Only 6 of 1,013 pulps returned gold values at or above 1 g/t. The second, by

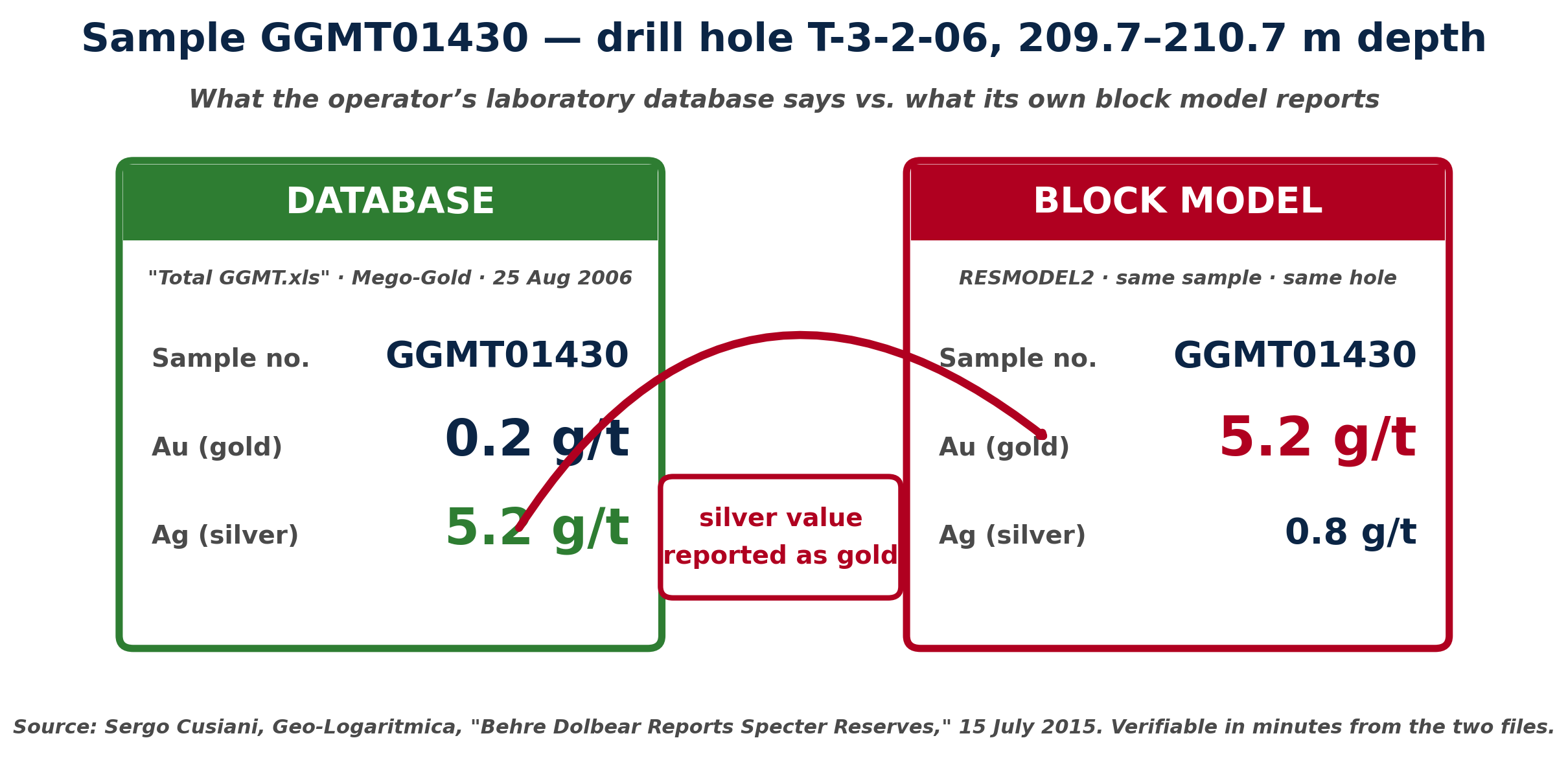

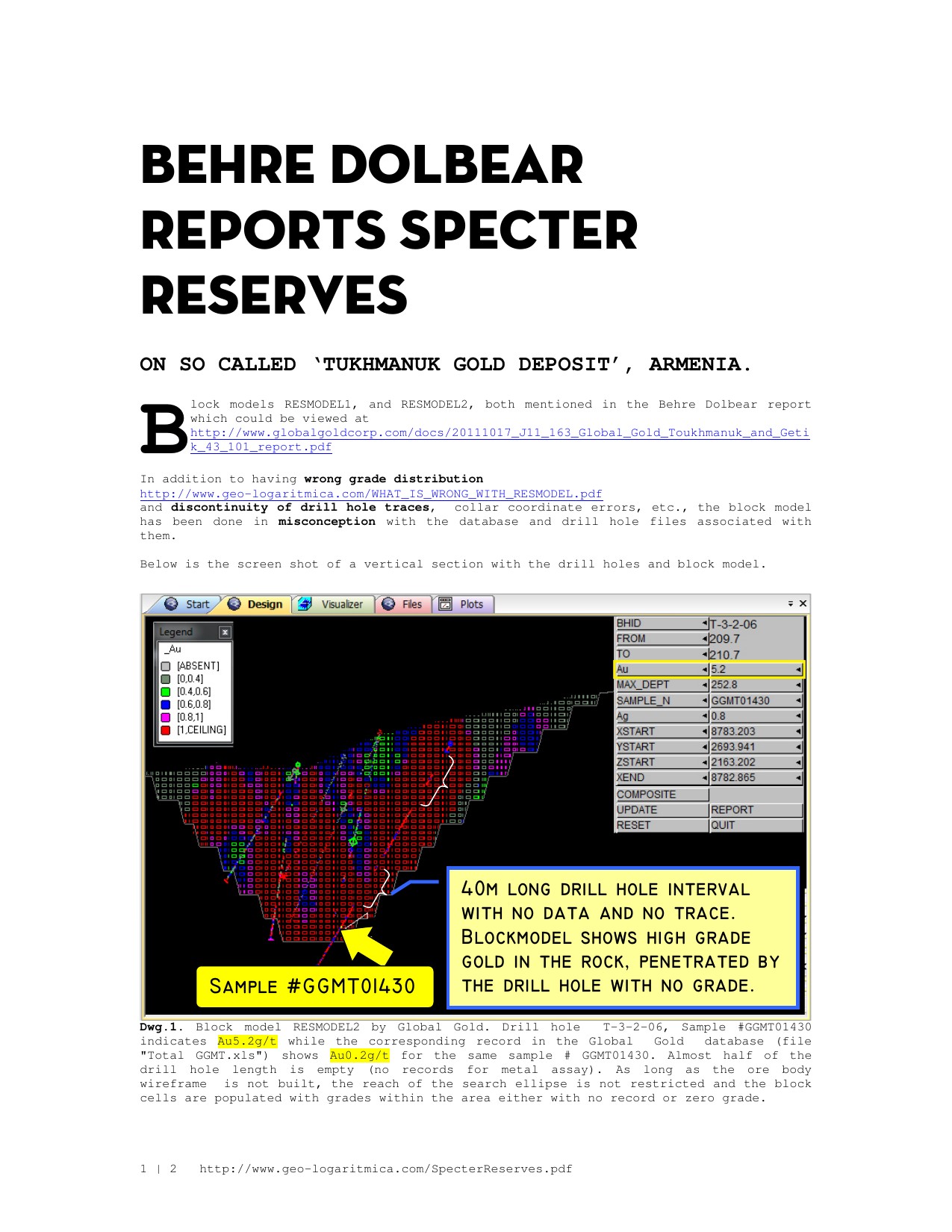

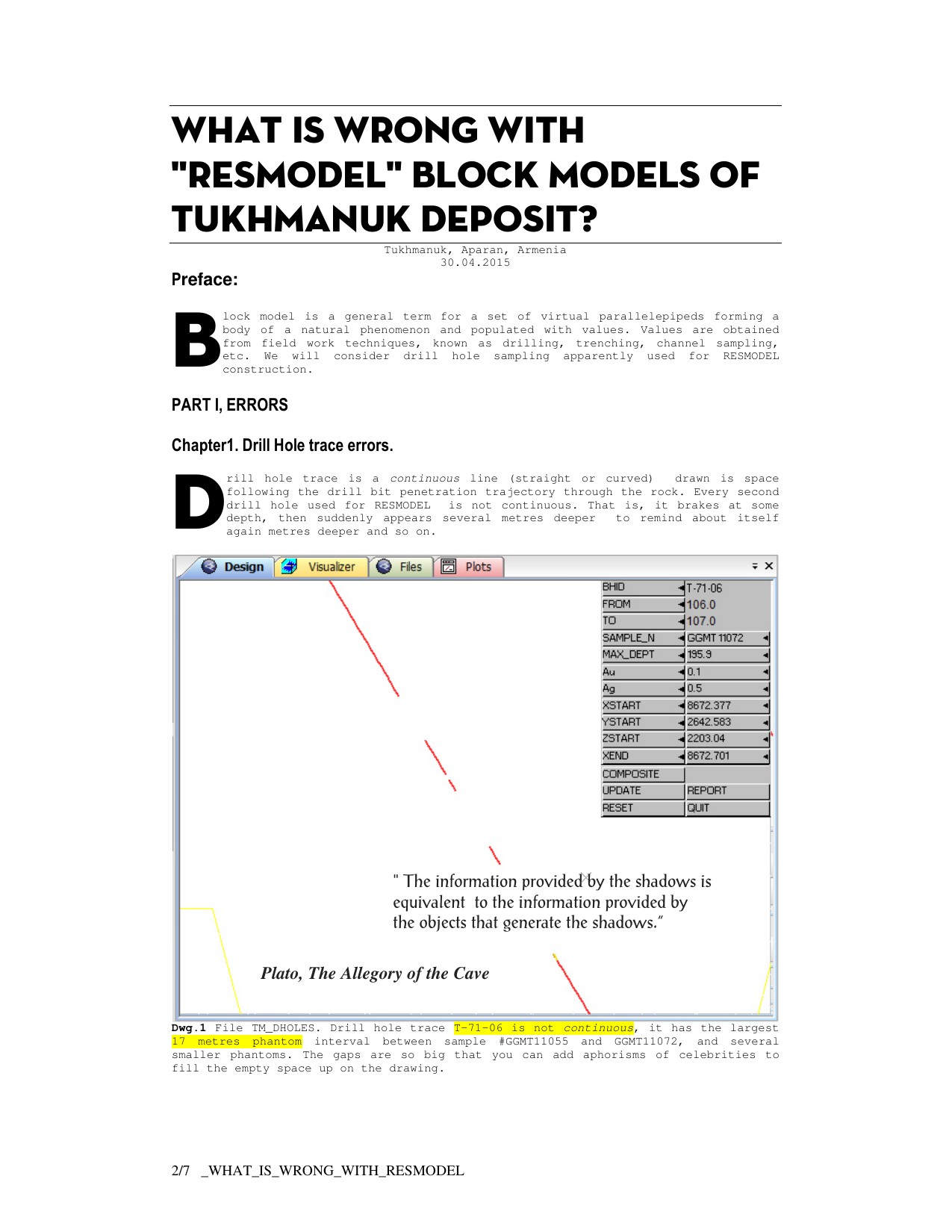

Sergo Cusiani of Geo-Logaritmica in 2014–2015, was a forensic

analysis of the RESMODEL block model itself. It identified

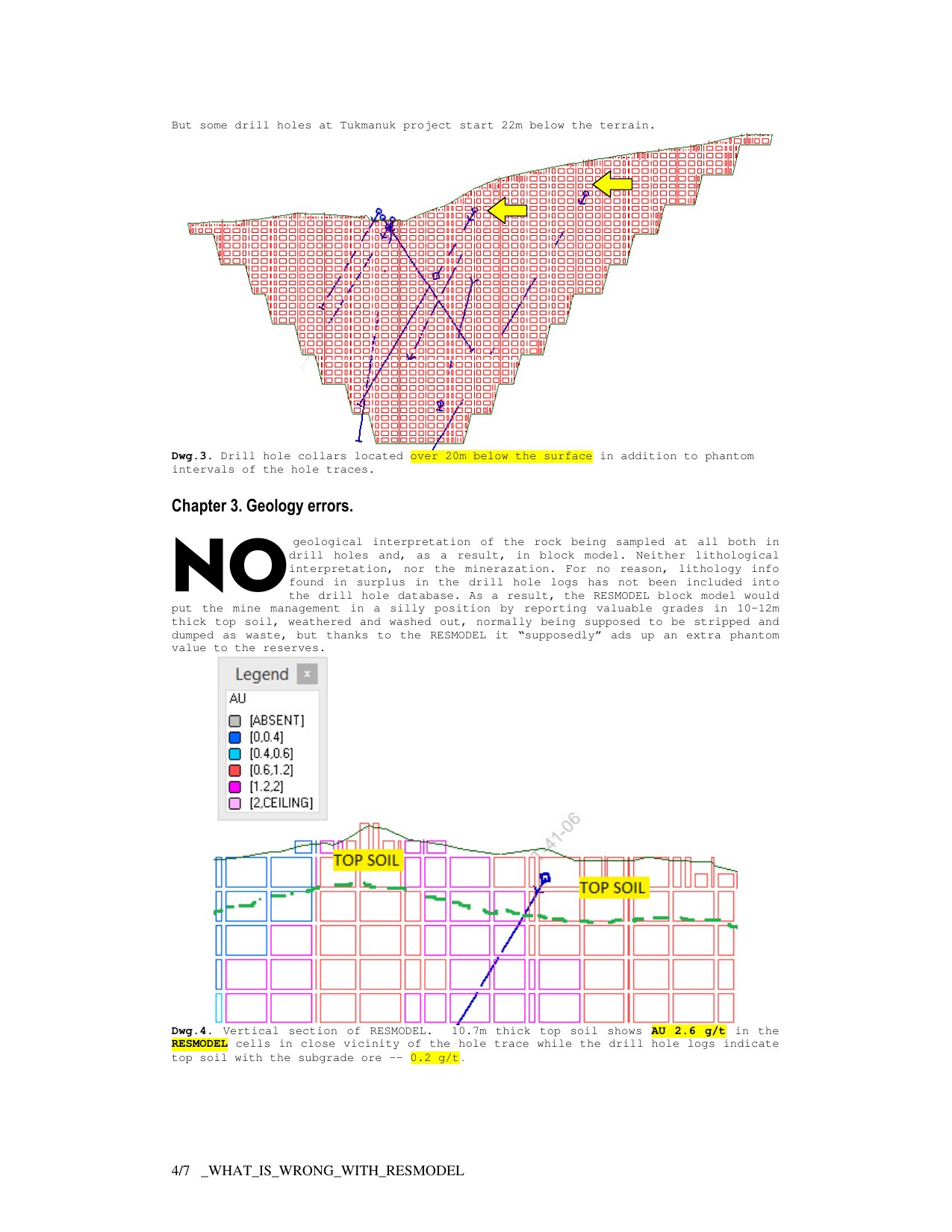

discontinuous

drill-hole traces, drill-hole collars placed twenty-two metres below the physical

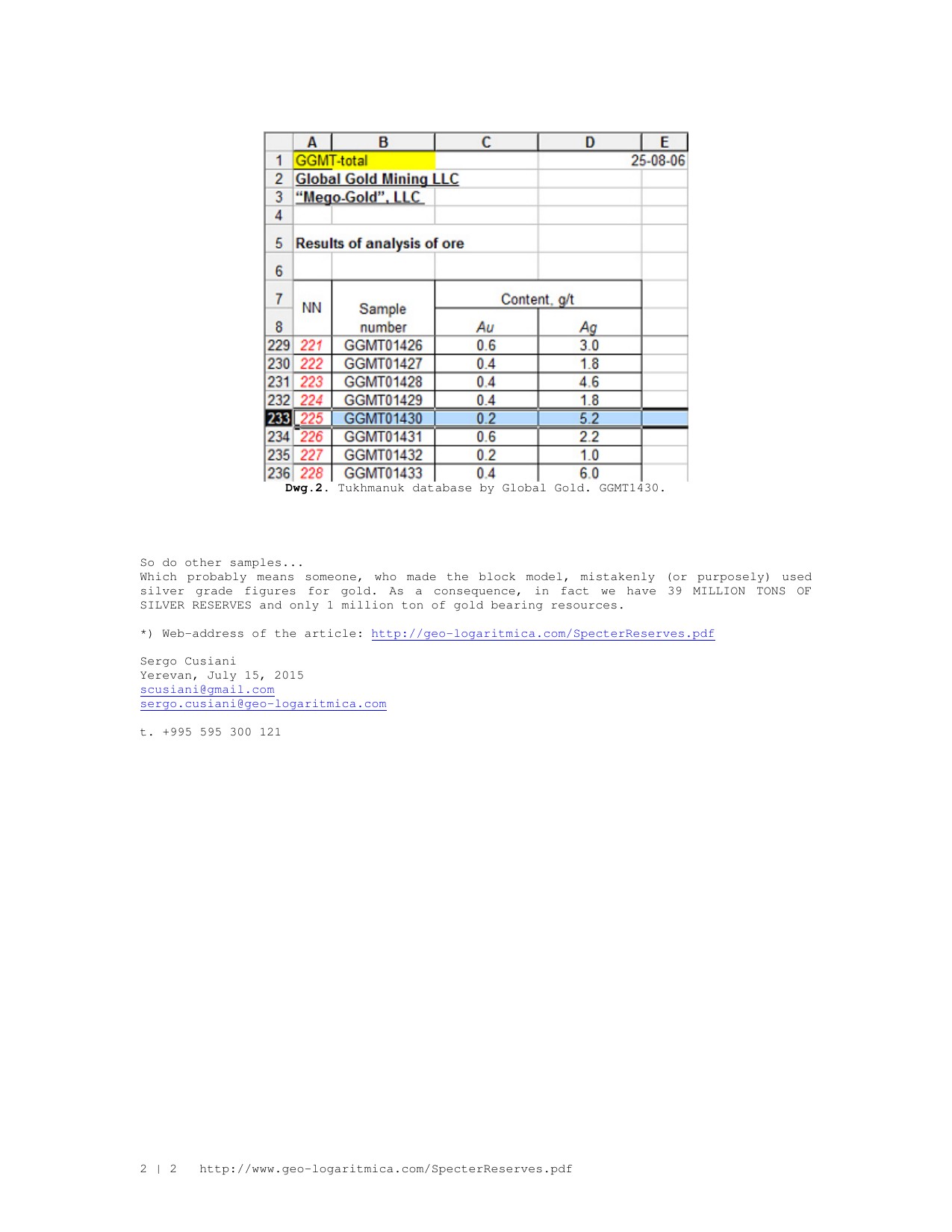

terrain, top-soil intervals reporting ore-grade gold, and — most consequentially

— a direct side-by-side demonstration, for a named sample on a named drill hole,

that the “gold” value in the block model was the silver

value from the operator’s own laboratory database.

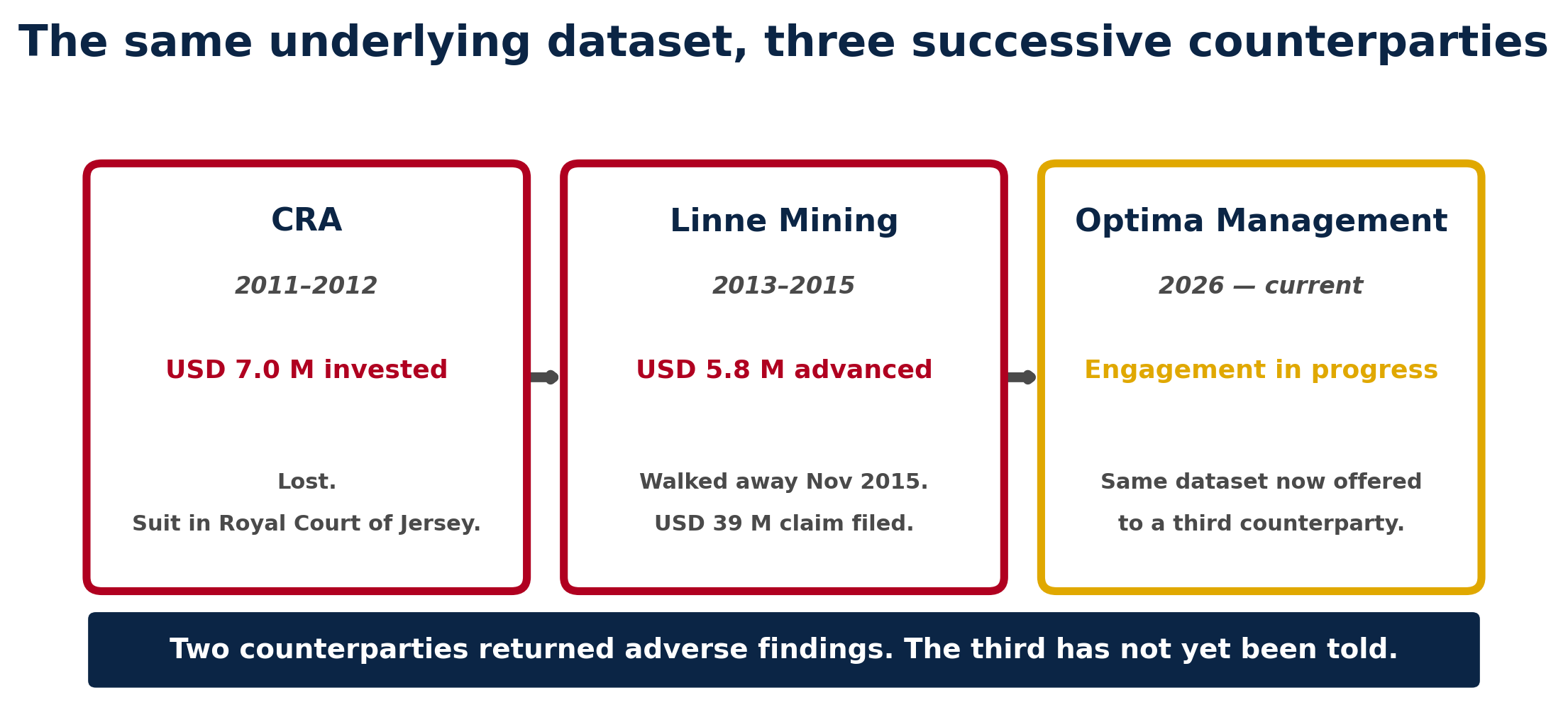

Consolidated Resources Armenia, the JV investor who commissioned the CSA work, lost its

USD 7 million investment and sued in the Royal Court of Jersey. Linne Mining, the

contract miner who commissioned the Cusiani work, walked away in November 2015, filed

a USD 39 million creditor claim in the Mego-Gold bankruptcy, and disappeared. Both

counterparties entered the transaction on the strength of the same assay database.

The 2016 GKZ register is the product of that same database, untouched.

The commissioning record is on paper. CSA Global’s Toukhmanuk engagement began

under Assignment Specification Agreement RAS.TRK.01,

signed on 18 November 2011 by Van Z. Krikorian as Chairman for

Global Gold Consolidated Resources Limited (Ogier House, St Helier, Jersey) and on

20 October 2011 by Malcolm Titley as Managing Director of CSA Global

(UK) Ltd. The agreed scope, in the agreement’s own terms, includes

“further QAQC review work and re-assaying”, laboratory audits of the

site laboratory and the primary check laboratory facilities, and

“NI-43-101 Compliant Mineral Resource Estimation and Reporting”. The

551-pair finding five months later was not a volunteered disclosure from outside:

it was the output of a programme the signing party had commissioned by name.

The fact that CSA produced what appears to be a negative report today only

increases the importance of transparency.

— Van Z. Krikorian, email, 20 April 2012, 17:21